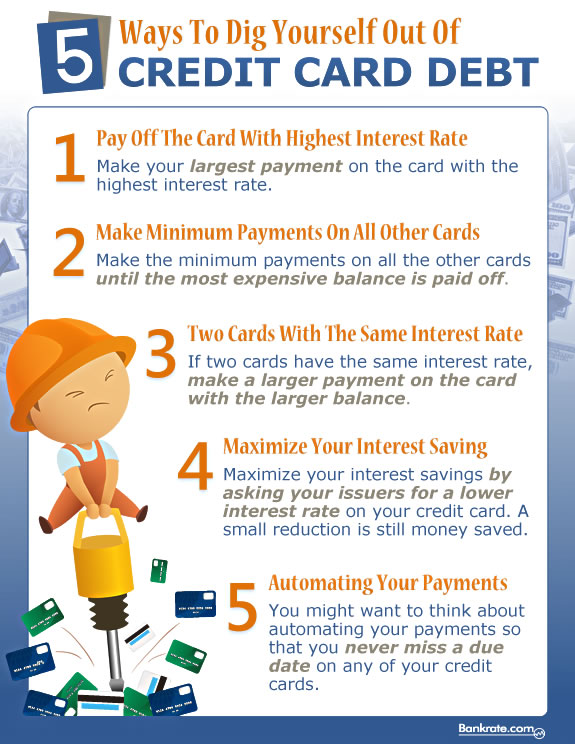

Some Of Financial Debt Solutions

= portion of overall debt owed overall debt Example: auto loan-- overall debt = $1,145.39/ $3,380.69 = 0.34 or 34 percent To figure out the quantity you can pay on each debt, make this estimation: total amount can pay X percentage of total debt owed = quantity can pay on that debt Example: $300 X. 34 Personal Debt = $102 Technique 3.

Financial obligations Amount owed Amountrequired Proratedpayment Auto loan $1,145.39 $180 X. 50 $90.00 Bank card 680.30 35 X. 50 17.50 Bank loan 525.00 170 X. 50 85.00 Bank loan 755.00 190 X. 50 95.00 Department shop 275.00 25 X. 50 12.50 Overalls $3,380.69 $600 $300.00 You have $300 per month available for debt payments.

Each lender is offered a prorated payment of half of the regular month-to-month payment. It is essential to repay all of the financial obligations you owe. If there is not sufficient cash to pay on all of your loans, consider prioritizing your debts. Financial obligations you might desire to pay very first consist of home mortgage or lease, utilities, protected loans, and insurance coverage.

Some examples of 3rd top priorities are physician, dental professional, and hospital bills. Member of the family and good friends typically want to wait. Use the worksheet sterlingdeweydsok.huicopper.com/financial-debt-solutions-poll-of-the-day on page 7 to establish your debt-payment strategy. Write the lender's name in the first column. Figure the portion of overall debt you owe each lender and compose it in the second column.

What Does Debt Management Do?

Choose if you will pay the debtors in equivalent amounts (Method 1), by proportions (Technique 2 or 3), or according to what action the financial institution may take (such as garnishment or repossession). Compose the dollar amount you can pay each creditor monthly in the fourth column. Now that you have worked out a strategy, destroy all of your credit cards.

Lenders typically are more responsive to your proposition if you take the initiative to contact them first and reveal a genuine desire Visit this page to pay your obligations. If you can not visit your creditor, call or write a letter. A sample letter you can use for writing your letter is consisted of in this publication.

In your letter, make sure to include the following: Why you fell behind in your payments (such as loss of job, disease, divorce, death in the family, or bad money-management abilities). Your current earnings. Your other obligations. How you plan to bring this debt up-to-date and keep it present. The exact quantity you will be able to pay back every month.

If you fail to follow the strategy you and your financial institutions have concurred upon, you harm your possibilities of getting future credit. Tell your lender about any modifications that may impact your payment contract. For extremely severe debt issues, a not-for-profit credit therapy firm might be able to even more negotiate lower regular monthly payments or interest.

The 20-Second Trick For Personal Debt

Customer Credit Therapy Provider (CCCS) companies in Mississippi https://en.wikipedia.org/wiki/?search=debt solutions include Finance International (statewide), Family Service Agency (Southaven), and Cred Capability (Jackson and statewide). Bankruptcy might be the last option in managing debt. The Federal Insolvency Code provides two types of debtor relief. Chapter 7 of the code is the straight bankruptcy provision and attends to liquidation (transform into money) of the debtor's properties.

Mississippi law lets the debtor keep particular property, and all other financial obligations are released in personal bankruptcy. With bankruptcy under Chapter 7, you quit the residential or commercial property you set up for collateral when https://www.washingtonpost.com/newssearch/?query=debt solutions utilizing credit unless the financial obligations are declared by court consent and you continue to pay the lender. Chapter 13 is the wage-earner's strategy.

While paying the financial obligations, you will have the ability to keep the things you bought on credit if the courts approve your strategy. Changes in personal bankruptcy laws entered into effect in October 2005. The changes offer more reward to seek personal bankruptcy relief under Chaper 13 instead of Chapter 7. If you have a consistent earnings, Chapter 13 lets you keep residential or commercial property you may otherwise lose.

After you have actually made all the payments under the plan, you recieve a discharge of your financial obligations. https://en.search.wordpress.com/?src=organic&q=debt solutions With minimal exceptions, the Bankruptcy Abuse Avoidance and Consumer Security Act of 2005 needs individuals who prepare to file for bankruptcy security to get credit counseing from a government-approved Financial Debt Solutions company within 180 days before they file.